Navigating Healthcare Options: Health Insurance 2024 Plans – Accessing Vital Healthcare Coverage

<meta name=Navigating Healthcare Options: Health Insurance 2024 Plans – Accessing Vital Healthcare Coverage>

Navigating Healthcare Options: 2024 Health Insurance Plans

Unlocking Access to Essential Healthcare Coverage

Hello, Smart People!

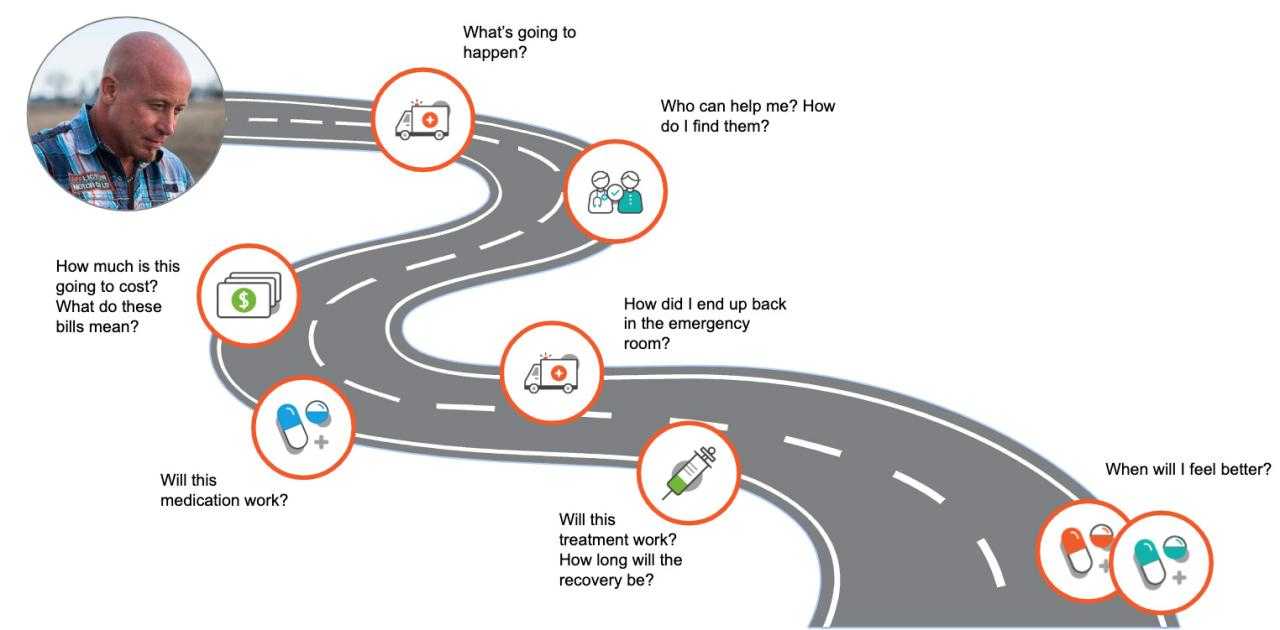

Navigating the complexities of healthcare can be an overwhelming task. The 2024 Health Insurance Plans aim to simplify this process, providing individuals and families with access to vital healthcare coverage. In this comprehensive guide, we will explore the benefits, challenges, and strategies for maximizing your healthcare options.

Understanding the Basics of Health Insurance

Health insurance is a form of financial protection that assists individuals in covering the costs of medical expenses. These expenses can include doctor’s visits, hospital stays, prescription drugs, and other healthcare services.

Health insurance plans are typically offered by insurance companies or through government programs such as Medicare and Medicaid.

Navigating the Marketplace

The Health Insurance Marketplace is a government-run website where individuals can compare and purchase health insurance plans. The Marketplace offers a variety of plans from different insurance companies, making it easier for individuals to find coverage that meets their needs and budget.

To be eligible for coverage through the Marketplace, you must meet certain income requirements and citizenship or residency status.

Types of Health Insurance Plans

There are several types of health insurance plans available, each with its own set of benefits and costs.

The most common types of health insurance plans include:

- Health Maintenance Organizations (HMOs)

- Preferred Provider Organizations (PPOs)

- Exclusive Provider Organizations (EPOs)

- Point-of-Service (POS) Plans

- High-Deductible Health Plans (HDHPs)

Choosing the Right Plan for Your Needs

Choosing the right health insurance plan can be a challenging task. It is important to consider your individual needs, budget, and health status.

Factors to consider when choosing a health insurance plan include:

- Monthly premiums

- Deductibles

- Copays

- Coinsurance

- Out-of-pocket maximums

- Network of providers

- Coverage for prescription drugs

Enrolling in a Health Insurance Plan

Once you have chosen a health insurance plan, you need to enroll in order to activate your coverage.

You can enroll in a health insurance plan through the Health Insurance Marketplace, directly through an insurance company, or through your employer.

Maximizing Your Coverage

Once you have enrolled in a health insurance plan, there are several steps you can take to maximize your coverage.

Tips for maximizing your health insurance coverage include:

- Understanding your plan benefits

- Using in-network providers

- Getting preventive care

- Managing your prescriptions

- Filing claims correctly

Conclusion

Navigating the healthcare system can be a complex process, but understanding the basics of health insurance can help you make informed decisions about your healthcare coverage.

By following the tips and strategies outlined in this guide, you can maximize your access to vital healthcare services and protect yourself and your loved ones from financial hardship.

Remember, healthcare is a right, not a privilege. Everyone deserves access to affordable, quality healthcare.

FAQs

What is the difference between an HMO and a PPO?

HMOs (Health Maintenance Organizations) typically have lower monthly premiums than PPOs (Preferred Provider Organizations), but they also have a more restrictive network of providers. PPOs offer more flexibility in choosing providers, but they typically have higher monthly premiums.

What is a deductible?

A deductible is the amount of money you have to pay out-of-pocket before your health insurance plan starts to cover costs. Deductibles can vary depending on the plan you choose.

What is a copay?

A copay is a fixed amount of money you pay for a specific healthcare service, such as a doctor’s visit or prescription drug.

What is coinsurance?

Coinsurance is a percentage of the cost of a healthcare service that you pay after you have met your deductible.

What is an out-of-pocket maximum?

An out-of-pocket maximum is the most you will have to pay for covered healthcare services in a year. Once you reach your out-of-pocket maximum, your health insurance plan will cover 100% of the costs of covered services.

What is a network of providers?

A network of providers is a group of healthcare providers who have contracted with an insurance company to provide services to its members. Using in-network providers typically costs less than using out-of-network providers.

What is covered by health insurance?

Health insurance typically covers a wide range of healthcare services, including doctor’s visits, hospital stays, prescription drugs, and preventive care.

How can I get help paying for health insurance?

There are a number of government programs that can help you pay for health insurance, such as Medicaid and the Children’s Health Insurance Program (CHIP). You may also be able to get help from your employer or through community organizations.

What should I do if I have a problem with my health insurance?

If you have a problem with your health insurance, you should contact your insurance company’s customer service department. You can also file a complaint with your state’s insurance commissioner.

How can I find a health insurance plan that meets my needs?

You can compare and purchase health insurance plans through the Health Insurance Marketplace or through an insurance company. You can also get help from a health insurance agent or broker.

What is the open enrollment period for health insurance?

The open enrollment period for health insurance is the time of year when you can enroll in or change your health insurance plan. The open enrollment period typically runs from November 1st to December 15th.

What happens if I don’t have health insurance?

If you don’t have health insurance, you could face financial penalties. You could also be responsible for paying the full cost of your medical care.

What are the benefits of having health insurance?

Health insurance offers a number of benefits, including:

- Access to affordable healthcare

- Protection from financial hardship

- Peace of mind